Journal Entries to Issue Stock Financial Accounting

We have now reached December, and the second and final call for class A shares is now coming due. We would repeat the journal entries we created for the first call. So for completeness of the example, the following journal entries would be made by ABC’s accounts team. The debit to the bank account reflects the $400,000 ABC now has from its first call on the class A shares. And the credit to the call account can now be closed as this money is no longer due from shareholders. As stated in the prospectus, the first call of 20 per cent is due from the Class A shareholders by September 30.

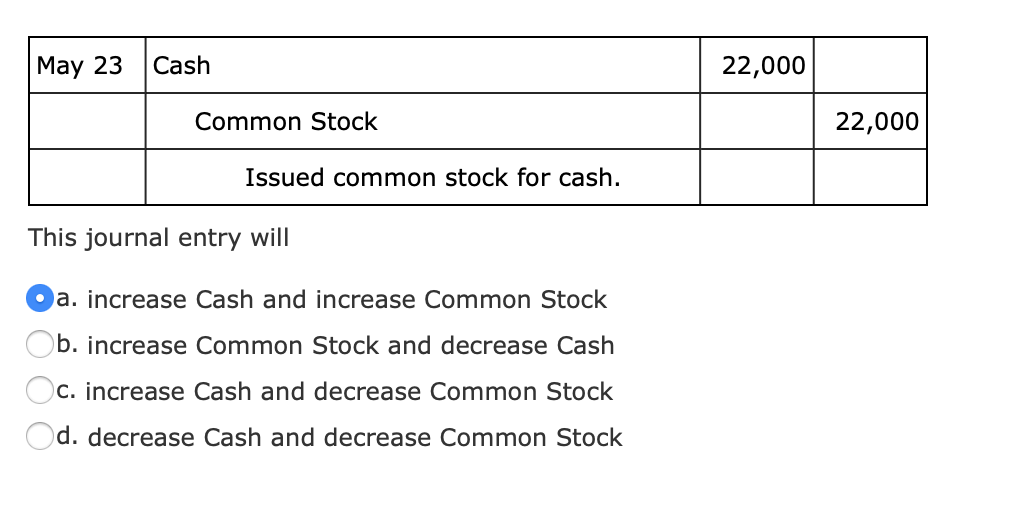

3: Issuing Stock for Cash

When stock is repurchased for retirement, the stock must beremoved from the accounts so that it is not reported on the balancesheet. The balance sheet will appear as if the stock was neverissued in the first place. Chad and Rick have successfully incorporated La Cantina and areready to issue common stock to themselves and the newly recruitedinvestors. Thecorporate charter of the corporation indicates that the par valueof its common stock is $1.50 per share. When stock is sold toinvestors, it is very rarely sold at par value. Stock with no par value that has beenassigned a stated value is treated very similarly to stock with apar value.

What are common shares?

Making the right entries on your books is crucial if your business offers equity to investors. The most common form of a stock split is 2-for-1 or 3-for-1, it means one share will be split into 2 or 3 share while the price of two or three share equal to one share before split. And as we know before, 5 per cent of this is the par value, and the remaining 95 per cent is the additional paid-in capital or premium the shareholders are paying above par value. The first debit entry takes the $400,000 in application money out of the application account. If then splits this across the Class A Share Capital account, being the allotted money. Then theClass A Additional Paid-in Capital account, as we calculated above.

Common Stock Issued for Non-Cash Exchange

When a company issues new common shares from treasury, it means that the company is creating and selling new shares that have not previously been outstanding. Treasury shares are authorized but not currently owned by anyone, so they are effectively “new” shares that the company is creating and selling to raise capital. Hence, we may come across the circumstance in which the common stock has no par value (e.i., no par value registered on the stock certificate). In this case, when we issue the common stock, we will need to record the entire amount of cash received to the common stock account without additional paid-in capital involved.

These features include the right to receive dividends and voting rights. Usually, the accounting for the issuance of a common stock involves three accounts. These include compensation, share capital and share premium accounts. For that, it is crucial to separate the par value of shares from the total finance received. The journal entries for the issuance of common stock impact three accounts. The first involves the debit side, which usually includes the account to record the compensation.

- It excludes the share that the company buyback from the market.

- However, states do allow the authorization to be raised if necessary.

- In each country, there are different laws and regulations that govern how shares can be traded and owned.

- This means that the stock is issued without assigning a stated value.

Assuming that the company XYZ still has a $100,000 outstanding balance of the additional paid-in capital account on the balance sheet before the issuance of these 10,000 shares of common stock. In this journal entry, both assets and equity increase by $20,000. Also, there is no additional paid-in capital as the company issues the stock at the par value. The company issues common stock for cash and the issue amount is more than the par value.

In the previous article, we covered the cost of comm stock equity calculation. In this article, we cover how to account for the issuance of common stock. This invoice for a freelance designer ranges from the journal entry for issuance of common stock of all types from par value stock to no par value stock as well as stock for non-cash assets.

However, the share capital account only holds the par value for the issued shares. Furthermore, this account doesn’t necessarily include the finance received from the issuance of shares. Selling common shares to investors is a common method for companies to raise capital.

This contrasts with issuing par value shares or shares with a stated value. In some states, the entire amount received for shares without par or stated value is the amount of legal capital. The legal capital in this example would then be equal to $ 250,000. The legal capital in this example would then be equal to $ 250,000. When it issues no-par stock with a stated value, a company carries the shares in the capital stock account at the stated value.

Common stock forms the basic ownership units of most corporations. The rights of the holders of common stock shares are normally set by state law but include voting for a board of directors to oversee current operations and future plans. Common stock usually has a par value although the meaning of this number has faded in importance over the decades. Upon issuance, common stock is recorded at par value with any amount received above that figure reported in an account such as capital in excess of par value. If issued for an asset or service instead of cash, the recording is based on the fair value of the shares given up. However, if that value is not available, the fair value of the asset or service is used.